What most people don’t know, is that a HSA can be an incredibly powerful investment vehicle. If you’ve completed the following steps, and have a HSA account, this post details why and how you should maximize and grow your HSA.

- Step 1: Building a Proper Emergency Fund

- Step 2: Get Your Employer Match (401k)

- Step 3: Pay Off All Debt (Except the House)

- Step 4: Max Out Your Roth IRA

What is an HSA?

If you’re enrolled in a High Deductible Health Insurance Plan, then you’re eligible to open a Health Savings Account (HSA). A HSA is a tax-free savings account used to save money specifically for medical expenses. Some of these future medical expenses include doctor and dental visits, therapy sessions, medical imaging and medical services.

The great thing about using a HSA for medical expenses is that you get a benefit that you don’t see with almost any other investment account. That benefit is the triple tax advantage. Your contributions are tax free. Your account growth is tax free. And, your withdrawals for medical expenses are tax free. This makes a HSA vital to controlling all medical expenses.

But, what usually gets forgotten is that your HSA can act as a traditional retirement account once you turn 65. So, if you’ve been diligent with growing your HSA, you’ll find out that it can be great in retirement even if your medical expenses remain low. Unlike with medical purchases, you do pay taxes on withdrawals after the age of 65 but that’s normal with a traditional retirement account.

It’s important to note that if your employer offers a HSA, you should use that rather than shopping around for a better HSA. The reason is you can then setup direct deposit with your employer which allows you to bypass FICA taxes at 7.65% (a benefit that IRA’s and 401k’s don’t even offer).

How much should I invest?

It’s simple. You should max out the allowable contributions your HSA. There are two main reasons for this:

- In retirement, medical expenses are usually some of your largest expenses. As you age, you tend to need more medical help and services which can get expensive quick. And, a HSA is the best way to pay for any medical expenses anyways (regardless of age).

- If you don’t end up needing all the money you’ve saved for medical expenses, you can use your HSA as a traditional retirement account. There aren’t any withdrawal requirements either which means you can withdraw from it whenever you want to.

In 2019, the annual contribution limit for a single plan is $3,500 while a family plan is $7,000. If you’re 55 or older, your contribution limit increases by $1,000.

In my case, where I’m on a single plan, I’ve setup monthly direct deposits with my employer that equal out to ~$291 per month. This way I’m guaranteed to hit the max contribution every year and avoid FICA taxes.

Where should I invest it?

First and foremost, I recommend you keep enough cash in your HSA to cover twice your annual deductible. For example, my annual deductible is $1,500. Therefore, I’ll always keep $3,000 of cash in my HSA before I start investing any amount greater than that.

Second, If you’ve been following my steps to financial independence (also referenced in this post’s intro), then you’ll know that I’ve recommended putting your 401k and IRA contributions into a target date fund. The target date funds I’ve suggested have a stake in mostly stocks and bonds. So, I like using my HSA to invest in real estate to add more diversification to my portfolio. What I’d recommend is finding out who your HSA plan is through, and then searching for the best Real Estate ETF that your plan offers. At that point, I plan on investing in Vanguard’s Real Estate ETF (VNQ) because of Vanguard’s supreme reputation and the fund’s very low expense ratio of 0.12%.

What is my HSA potential?

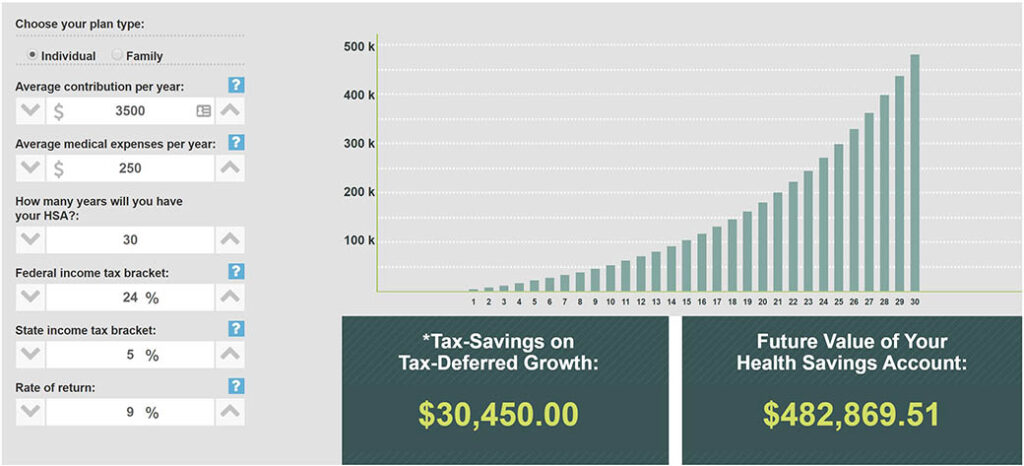

Your HSA has the potential to grow into a significant amount of money. If you were to max out your HSA for 30 years, withdraw $250 from it annually for regular medical expenses, and grow the rest using a Real Estate ETF that averages a 9% return, then the future value of your HSA will be nearly $500,000. With that amount of money in retirement, you shouldn’t need to worry about rising medical costs and unexpected medical emergencies. You’ll also have enough money to supplement your retirement income to live a secure and prosperous life. Check out the graphic below that shows the growth of your HSA over 30 years to reach nearly $500,000. (HSA Savings Calculator)

I just opened my HSA late last year after realizing all the benefits listed in this blog. Since then I’ve setup automatic monthly contributions that put me on track to max out my HSA every year. Currently, my HSA sits at $2,400 which will cover many major unexpected medical costs for the next year or so. In addition, I see it as the start of my half million dollar plan to eliminate medical expense worries and supplement my future retirement.

Summary

If you didn’t know much about a HSA or haven’t realized the benefits before this post, I hope you understand it’s great potential now. HSA’s are the best way to pay for medical expenses now and in the future. They’re also just as beneficial when used as a traditional retirement vehicle.

If your plan is eligible, I recommend you open a HSA with your employer. Setup direct deposits of $291 per month. Once you’ve saved enough to cover your deductible twice, invest everything else in a Real Estate ETF. Next thing you know, medical worries will be a thing of the past and a financially stable retirement will be your future.

If you liked this post, please subscribe to the weekly newsletter and follow the social media accounts for the latest content!

Disclosure: I frequently review or recommend products and services that I own and use. If you buy these products or services using the links on this site, I receive a small referral commission. This doesn’t impact my review or recommendation.