It was May of 2013 when I got my first internship after attending the Rochester Institute of Technology. And it was a significant moment for me. A lot bigger than I ever expected it to be. It was a moment that flipped my perspective entirely. I was no longer spending money to learn and an acquire a degree. I was now working to earn an income and build a life I would enjoy. I was finally taking a step in the life that all my time in college had prepared me for. And what happened was something I had never expected. A mountain of debt welcomed me immediately.

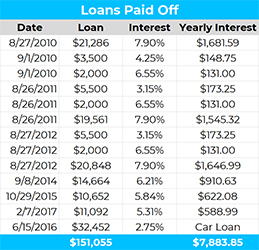

For the first time that I can really remember, I looked at my student loans. I know that seems odd, but I just can’t remember ever worrying about finances while I took classes. I knew that everything was being paid for by loans, but I never thought about what they were or when I’d have to pay them back. It sounds so stupid now, but I was oblivious to it. And in May of 2013 I saw a list of loans totaling around $90,000. And if that weren’t bad enough, those loans would now start accruing nearly $6,000 of interest per year automatically. And while my $15 per hour internship seemed decent at the time, I now realized that paying $6,000 per year to my loans wouldn’t even decrease my balance. It’d maintain it.

And this moment played a significant role in my life. I wasn’t working to earn an income and build a life as I previously thought I would be. I was working for money that wasn’t mine. My hours on the job led to cash that I wouldn’t ever see. And I was indebted to banks for what appeared to be forever… so, I did what any intelligent kid would do. I went back to RIT for my master’s degree and accumulated another $40,000 of debt.

And I’m not writing this post to hate on college. My undergraduate and graduate degrees have provided me with a phenomenal education that’s led to a lucrative and enjoyable career. And I don’t regret any of it and I’d do it all again. But, as I sit here debt-free today, I still remember the long arduous road that got me here. I remember checking in with my doctor for depression as my life seemed hopeless. I remember crying in bed wishing I could fast forward my life to a spot where debt didn’t exist. But this journey forced me to become financially literate. It forced me to become financially responsible. And it forced me to create excellent financial habits that not only led me to pay off $150,000 of debt but is now leading me to create long term wealth. And today, I’m going to detail how I paid off all that debt in less than 10 years. Let’s get into it!

Put a Plan Together

The first thing I needed to do was put together a plan. Like I mentioned, I knew I had loans throughout college, but I didn’t know how many or how much or their interest rates. So, I immediately put together a quick spreadsheet that listed out every loan I had, the total loan amount, the interest rate, and the minimum monthly payments. Once I had this, I knew the minimum monthly payments I’d need to make.

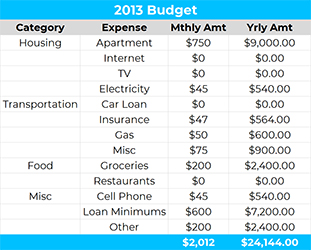

I could then put together a budget that showed my total monthly income and total monthly expenses which now included the loan payments. But by now you all know me. I don’t want to live by minimums I want to live by optimals. There’s no way I wanted to live with this looming debt for decades of my life. I wanted it gone as soon as possible to get back to building a life I would enjoy. And so, I was determined to pay off more than the minimums whenever I could. And I have an article dedicated to What Order To Pay Off Your Debts if you’re interested in that. I personally chose the avalanche method by sending my extra loan payments to the loan with the largest interest rate. This is mathematically the quickest way to pay off your debts but can be much more daunting and less motivating than the snowball method which requires you to send extra loan payments to the loan with the smallest balance first. But choose whatever way works best for you as there isn’t an enormous difference.

Decrease Expenses

Now the easiest way for me to increase my loan payments was to cut my expenses. By spending less, I would have more money available to pay off the loans. So, I got a cheap apartment that already included Wi-Fi and TV at $750/month. If I was savvier, I would’ve gotten a roommate and if my parents lived closer to Rochester, I would’ve moved back in with them. Both options would’ve saved me a lot more money. Either way, I picked an apartment that was less than a mile from where I worked to reduce my gas bill and minimize my time spent driving. I also didn’t pay for subscription services like Netflix, Disney Plus, or Hulu. I didn’t order out, schedule food delivery, or eat at restaurants. I didn’t frequent bars or have expensive hobbies. I did whatever I could to reduce my spending.

And surprisingly, I look back at this time and don’t regret any of it. I found other ways to have fun and entertain myself that were free like hiking, running, exercising, and exploring around town. It wasn’t nearly as bad as it sounds. And by minimizing your expenses, many people can find an extra five, then, or even twenty thousand dollars per year that could be used for dept repayment.

Increase Income

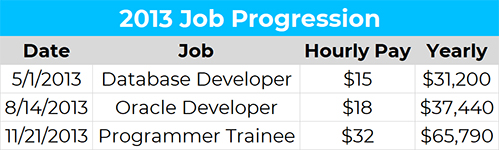

But you can only cut costs so much. You likely need shelter, transportation, and food to survive. At minimum, you’re still living off of at least $15,000 per year. And so, the only other way to pay back your loans significantly faster is to increase your income. And while this is easier said than done, it’s very possible. And unlike cutting your expenses, your income potential is unlimited. My first 3-month internship started at $15/hour and my second internship at $18/hour. I was then hired full-time in 2013 by my second internship employer with a starting salary of $65,000 which is a lot. But there was a lot of effort that I put in outside of work to get that first full-time job and to acquire raises and promotions since then. Most of my time spent after work was at home working on my master’s degree or on work related certifications. I acquired certifications in project management, cybersecurity, network administration, and database administration. I knew I needed more skills to acquire higher paying jobs and I spent a lot of time focusing on skill acquisition. Not only have I put a lot of effort into skill acquisition, but I’ve also focused on achieving the goals set by my employer. I think it’s always important to know what your current employer finds valuable, and then to excel at that. This will inevitably put you in a great position for raises and promotions.

And the reason I’m mentioning this is because paying off significant amounts of debt in a brief period of time isn’t possible by cutting costs alone. You need to focus on increasing your income. And this can be done many ways like skill acquisition or raise negotiation or switching jobs or getting a side hustle or working a second job. Or even a third as my sister does. And I’m not saying you need to maintain this gazelle intensity forever as Dave Ramsey puts it, but you need to have this intensity while you still have loans. These loans and their interest will eat away at you and financial future. And it’s worth doing everything you can to get out of this hole.

Final Thoughts

For around 7 years I was strapped with substantial amounts of debt from student loans and my car. At that time, all the money I made from working wasn’t mine. I never saw it. It went straight to the banks. And it was hard to live like this where I felt like no matter how hard I tried I wasn’t making progress. But by putting a plan in place I could at least get an idea of the finish line. I then cut my expenses that were holding me back and did whatever I could to increase my income and accelerate the process. Now 10 years later, I’m debt-free and using this same method to store away money for early retirement. And despite it being a tough long road, it’s been worth it. The experiences, the lessons, and financial habits have somehow been worth a lot more than the $150,000 of debt. And I hope sharing my story with you can help in wherever you’re at in the journey of debt repayment.

Looking for the top three things I’ve read, watched, and listened to this week? Check out my free health kit and weekly newsletter.

Watch a YouTube Video Summarizing the Post

Hey, I am Brandon Zerbe

Welcome to myHealthSciences! My goal has always been to increase quality-of-life with healthy habits that are sustainable, efficient, and effective. I do this by covering topics like Fitness, Nutrition, Sleep, Cognition, Finance and Minimalism. You can read more about me here.

Sources: