So, I’ve been pondering my financial future and attempting to determine how much I need to save to become financially independent. Financial independence meaning, I can live entirely off my investment without needing a job to sustain my lifestyle costs. Or how much money I need until I can live in my bedroom fulltime creating YouTube videos without any subscriber growth and still afford my organic plant-based dinners. This is more commonly known as retirement or my typical weekends. Traditionally, the 4% rule has been the basis for many retirement calculations but in 2021 with interest rates near zero, inflation spiking, and bonds producing little-to-no return, is this rule now too risky? What is the 4% rule and how much money do I need to retire? And what organic plant-based meal did I have for dinner last night that my 4% rule needs to account for? Well, let’s get into it!

The 4% Rule

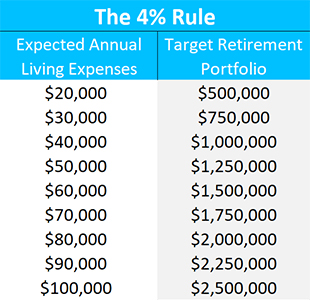

The 4% rule is a rule of thumb used to determine how much money you can safely withdraw in retirement each year from your total savings and not run out money before you die. And this rule was popularized by the Trinity Study which ran many retirement simulations on portfolios between the years of 1925-1995. And what they found, was that even in the worst years to retire, when the market performed its worst, the constant 4% withdraw rate in retirement nearly guaranteed that you’d never run out of money. And based on this study, many financial advisors and planners have used this rule of thumb to guide client’s retirement plans. So, for example, if you think your retirement lifestyle will cost $40,000 per year, then you’d need a $1,000,000 portfolio to hit that 4% withdraw rate and never run out of money. And below is a chart showing how much money you’d need in your portfolio based upon your expected living expenses. But this 4% rule was created in the 1990’s and based on strict guidelines that you likely won’t follow in reality. And with the market conditions, it now begs the question, is the 4% rule too risky?

The 4% Rule is Too Risky

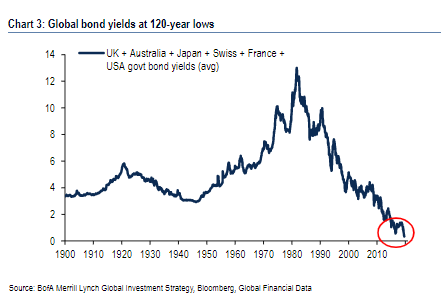

The 4% rule was established back when everyone planned for a set 30-year retirement and their portfolios were made up of around 60% stocks and 40% bonds. And when the simulations were run, bonds were producing a much higher rate of return than today. Historically, bonds averaged a rate of return of around 5-6% compared to less than 3% today. What this means is that most portfolios have shifted their allocations to more stocks and less bonds, for example 75% stocks and 25% bonds, to achieve the same rate of return previously. This requires taking on more risk than was previously calculated. Moreover, Vanguard and many other investment firms have projected that future returns on stocks will be significantly less than the historical averages. Just because the market has historically returned 10% per year on average, doesn’t mean it will continue that trend for the next 100 years. This could could mean that no matter your portfolio allocation, if the projections are correct, the 4% return is not going to cut it.

On top of that, while most people are planning for a 30-year retirement still, say retiring at 60 and living until 90, this doesn’t fit all situations. For example, the 4% rule assumes that after 30 years of retirement, your total savings will be all but depleted. While you’ll have enough money to make it until death, it could get scary the last few years with your healthcare costs rising and money dwindling. On top of that, you’ll leave no money left for your children to inherit or to donate to charity. And, if you’re planning to retire early and needing your savings to last you 40, 50, or 60 years, then you’d be in trouble. I mean if you follow the myHealthSciences protocol, you may be living it up to 100 and in good health! So, this is where the 4% rule starts to appear like a risky target. Plus, the 4% rule doesn’t take into consideration the additional taxes, expense ratios, and transaction costs which can make that 4% withdraw look more like a 3.79% withdraw rate requiring more total savings before you can retire. This has led several people to recommend a 2-3% withdraw rate to account for all the differences now in 2021 compared to back in the 1990’s. But not so fast. Let’s look at some of the other components not taken into consideration when the 4% rule was created.

The 4% Rule is Too Conservative

The 4% rule was a conservative number at the time it was created. It was designed to nearly guarantee that everyone would make it through retirement even if you retired at the worst possible time. This means, if you don’t retire at the worst possible time, like right before a market crash, your 4% withdraw rate will leave you with a ton of money leftover at the end of life. In many cases, the vast majority of people could use a 5-6% withdraw rate and be completely fine even with slightly lower returns, taxes, expense ratios, and transaction costs.

And let’s talk about spending. The 4% rule, for the sake of simplicity, assumes you withdraw 4% of your savings every year of retirement no matter what. This is called static spending. But most people will be better off using a dynamic spending strategy in retirement. When the stock market does well with a 15% rate of return, and inflation is low, you could feel much better withdrawing 7-8% of your portfolio. And when the market doesn’t do well with a -10% rate of return, or inflation is high, you could ease back your spending to a 3% withdraw rate to account for the tighter times. So, by adjusting your spending based on the market conditions, which most people can do in retirement, that 4% rule can be quite conservative.

To add onto that, this 4% rules takes into consideration only the money you’ve accumulated through 401ks, IRAs, Brokerage, or Savings accounts. It doesn’t take into consideration pensions or social security. And while I wouldn’t count or depend on pensions or social security, those that do get it will see around $20,000 per year in benefits that the 4% rule doesn’t account for making that 4% rule look even more conservative. From this standpoint, a 5-6% withdraw rate appears more useful. So, how am I attacking this?

This Chart Sums It Up Best

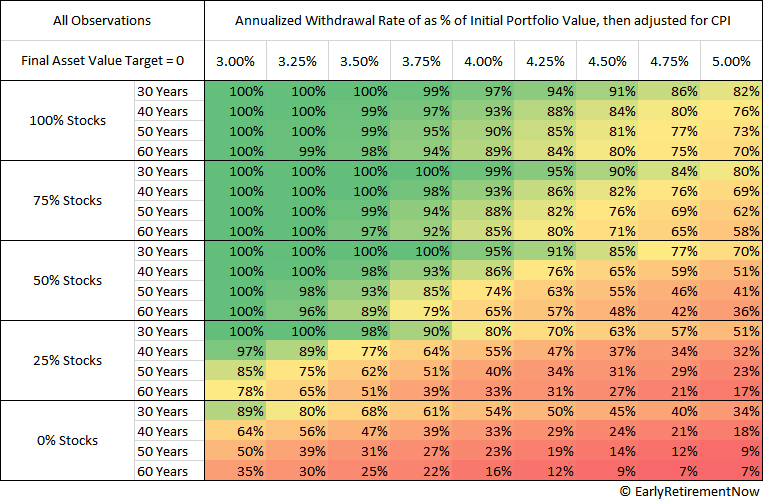

Well, Karsten Jeske who runs EarlyRetirementNow.com created a chart that I’ve found extremely useful. This chart takes into consideration how risky you want to be with your asset allocation (stocks vs bonds), how many years of retirement you’re shooting for (30, 40, 50, or 60), and provides calculations for various withdrawal rates. This chart gives you a more personal guide in determining what your future withdrawal rate could be, that allows you to better plan for retirement. Now, like I mentioned, this chart is still a rule of thumb that can be used to estimate how much you need for retirement as your actual withdrawals in retirement will be different than you’re currently planning. But either way, I like this chart for planning purposes.

For me, the creator and follower of the evidence-based myHealthSciences lifestyle designed to increase healthspan and lifespan to its greatest potential, I’m probably going to live to 150. But for the sake of relatability, let’s say I live to 100 and plan to retire early at age 40. In this case, I’m looking at 60 years of retirement. I am more risk seeking so I’d assume a 75% stock to 25% bond ratio. With those components, I’d like to assume near 100% certainty of having enough money to sustain my lifestyle without any stress at the end of life. Plus, as long as I don’t retire at the worst possible time, it’d be nice to have some insurance that there will be money left over for my kids or charitable donations. With these parameters defined, I can now use 3.25% as my target withdrawal rate. Now obviously, your situation is going to be different but that’s what great about this chart. It lets you get a better idea of what your withdraw rate should be in retirement. I can then do some quick math and say that if I want to live a $65,000 lifestyle in retirement, using the 3.25% withdraw rate, I’ll need to save up around $2 million in retirement. Now, can I hit a 2-million-dollar portfolio by age 40? Challenge accepted.

Final Thoughts

The 4% rule was created years ago when bonds had a higher rate of return, 30-year retirement plans were the default, and taxes, expense ratios, and transaction costs weren’t included. Thus, making the 4% rule look much riskier today. But the 4% rule also doesn’t take into consideration the average retirement date, dynamic spending, and additional money through pensions and social security. Thus, making the 4% rule look oppositely conservative. Luckily, Karsten created a useful chart to better estimate your personal withdrawal rate depending on your circumstances. And for me, after inputting my parameters, I’ve determined a 3.25% withdrawal rate to be a useful figure for me. But who knows! Retirement is so far away, and this could all change with kids, a wife, my job, market conditions, and my passions. Either way, it’s a useful north star to start planning my financial journey. Thanks for stopping by and look forward to sharing with you again next week!

And by the way, stick around for that organic plant-based dinner recipe that my retirement needs to fund. The perfect dinner recipe will be out soon!

Want a weekly update on the 3 most important things I’ve read, watched, and listened to within the past week?

Watch a YouTube Video Summarizing the Post

Hey, I am Brandon Zerbe

Welcome to myHealthSciences! My goal has always been to increase quality-of-life with healthy habits that are sustainable, efficient, and effective. I do this by covering topics like Fitness, Nutrition, Sleep, Cognition, Finance and Minimalism. You can read more about me here.

Sources: